- What is the Treasury Stock Method?

- How to Calculate Treasury Stock Method (TSM)

- Treasury Stock Method Formula

- Treasury Stock Method (TSM) Calculator â Excel Template

- 1. Operating Assumptions

- 2. Diluted EPS Calculation Example

- 3. Treasury Stock Method Calculation Example (TSM)

- 4. Treasury Stock Method Analysis (TSM)

What is the Treasury Stock Method?

The Treasury Stock Method (TSM) is used to compute the net new number of shares from potentially dilutive securities.

The underlying intuition behind the treasury stock method is that securities, such as options and warrants, that can be exercised should be accounted for in the total share count calculation.

In effect, the TSM estimates the hypothetical impact of the exercising of in-the-money securities to measure their collective effect on the fully diluted shares outstanding.

- The treasury stock method (TSM) is utilized to determine the net new share count from potentially dilutive securities, such as options and warrants, resulting in fully diluted shares outstanding (FDSO).

- The treasury stock method (TSM) assumes that the cash proceeds from exercising these dilutive securities are used to repurchase shares, thereby mitigating the dilution effect on existing shareholders.

- The formula to calculate fully diluted shares outstanding under the treasury stock method (TSM) starts with the total number of basic shares and adjusts for the new shares issued from the exercise of in-the-money options, leading to a more accurate representation of a company’s equity value per share.

- The treasury stock method (TSM) comprises summing the in-the-money options, calculating the shares repurchased with option proceeds, and determining net dilution to arrive at the total diluted shares outstanding.

- The inclusion of dilutive securities in the total diluted share count causes a reduction to diluted earnings per share (EPS).

How to Calculate Treasury Stock Method (TSM)

Under the treasury stock method (TSM) approach, the total diluted share count takes into account the new shares issued by the exercising of options and other dilutive securities that are “in-the-money” (i.e., the current share price is greater than the exercise price of the option/warrant/grant/etc.).

Conceptually, the treasury stock method (TSM) approximates what a company’s earnings per share (EPS) would be under the assumption that its dilutive securities are exercised.

The next core assumption inherent to the TSM is that the cash proceeds from the exercising of these dilutive securities (i.e., option proceeds) are then used to repurchase shares under the belief that a rational company would attempt to mitigate the dilutive impact of the options by doing so.

Unlike the calculation of basic shares outstanding and the coinciding basic earnings per share (EPS) metric, the diluted shares outstanding calculation under the treasury stock method (TSM) considers the potentially dilutive securities such as options, warrants, and convertible debt.

Hence, the fully diluted shares outstanding count is a relatively more accurate representation of the actual equity ownership and equity value per share of a company.

The exclusion of these types of securities into common equity would mistakenly inflate the earnings per share (EPS) figure.

Treasury Stock Method Formula

The treasury stock method formula to calculate the total number of diluted shares outstanding consists of all basic shares, and the new shares from the hypothetical exercise of “in-the-money” options and conversion of convertible securities.

Here, the number of shares repurchased is equal to the option proceeds (the number of gross “in-the-money” dilutive securities multiplied by the strike price) divided by the current share price.

Besides options, other examples of dilutive securities include warrants and restricted stock units (RSUs).

- Warrants → Similar financial instruments to options but result in the issuance of new shares if exercised

- Restricted Stock Units (RSUs) → Issued to the company’s management team with a convertible feature attached.

If disclosed, options are evaluated on a tranche-by-tranche basis to determine if they are “in the money.”

Each tranche has a strike price, which the option holder must pay to exercise the option as part of the contractual agreement.

- “In-the-Money” Options ➝ Strike Price < Current Share Price

- “At-the-Money” Options ➝ Strike Price = Current Share Price

- “Out-of-the-Money” Options ➝ Strike Price > Current Share Price

Furthermore, the EPS formula divides the net income of a company by its share count, which can be either on a basic or diluted basis.

That said, if a company has issued such securities in the past (i.e., the potential for conversion), its diluted EPS in all likelihood is going to be lower than its basic EPS.

The reason is that the denominator (the share count) has increased, whereas its numerator (net income) remains constant.

In terms of the steps involved in the TSM, first, the number of in-the-money options and other dilutive securities are summed up, and that figure is then added to the number of basic shares outstanding.

Note that only the securities deemed “in-the-money” are assumed to have been exercised, therefore those “out-of-the-money” are not included in the new share count.

In the subsequent step, the TSM assumes the entirety of the proceeds from the exercising of those dilutive options goes towards repurchasing stock at the current market share price. The assumption here is that the company would repurchase its shares in the open market to reduce the net dilutive impact.

Insider’s Tip: Exercisable vs. Outstanding Options

Companies oftentimes disclose both their “outstanding” and “exercisable” options, since certain outstanding options will have yet to vest.

For a long time, it was considered standard to include only the number of options and dilutive securities that are exercisable in the calculation of diluted shares, as opposed to outstanding.

However, the case could be made that to be more conservative in the diluted share count calculation, the number of outstanding options should be used despite not all being exercisable on the date of the valuation. This is done to reflect the reality that the majority of unvested options have a high probability of vesting someday, which is a practice that investors and firms have increasingly adopted in recent years.

Another minor complexity to be aware of is the tax benefit stemming from the elimination of interest expense or dividends associated with convertible securities (e.g., convertible debt) and preferred equity.

Treasury Stock Method (TSM) Calculator — Excel Template

We’ll now move to a modeling exercise, which you can access by filling out the form below.

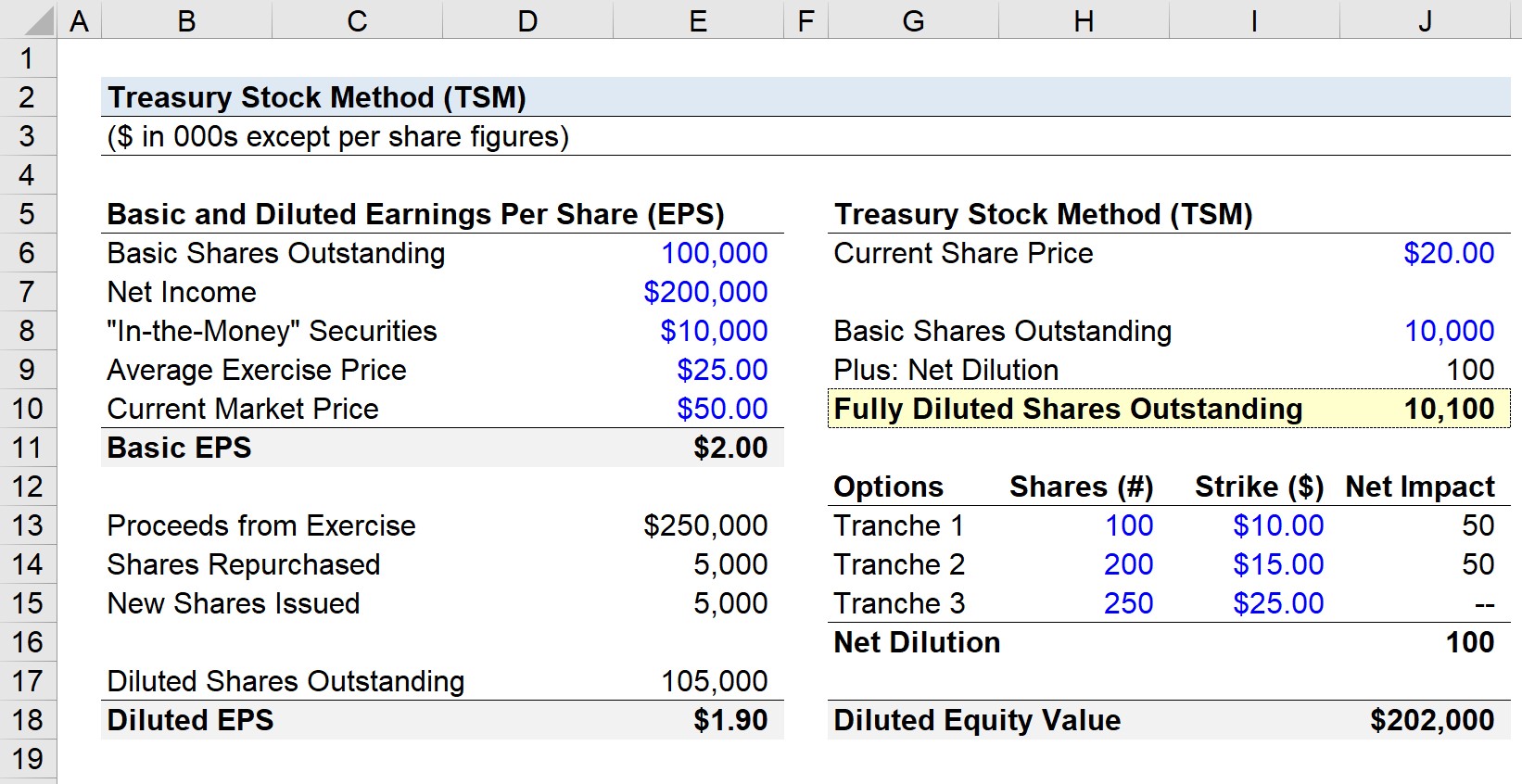

1. Operating Assumptions

Suppose a company has 100,000 common shares outstanding and $200,000 in net income in the last twelve months (LTM).

- Common Shares Outstanding = 100,000

- LTM Net Income = $200,000

If we were calculating the basic EPS, which excludes the impact of dilutive securities, the EPS would be $2.00.

- Basic EPS = 200,000 ÷ 100,000 = $2.00

But since we must account for the ITM securities not yet exercised, we multiply the potential shares issued by the average exercise price to get the total proceeds assuming they were exercised by the holder, which we calculate as $250,000 (10,000 multiplied by the exercise price of $25.00).

Upon dividing the exercise proceeds of $250,000 by the current market share price of $50.00, we get 5,000 as the number of shares repurchased.

We can then subtract the 5,000 shares repurchased from the 10,000 new securities created to arrive at 5,000 shares as the net dilution (i.e., the number of new shares post-repurchase).

- Net Dilution = 5,000

- Diluted Shares Outstanding = 105,000

2. Diluted EPS Calculation Example

After dividing the net income of $200,000 by the diluted share count of 105,000, we arrive at a diluted earnings per share (EPS) of $1.90.

- Diluted Earnings per Share (EPS) = $200,000 ÷ 105,000 = $1.90

In comparison to our starting point, the basic EPS of $2.00, and the diluted EPS is $0.10 less.

3. Treasury Stock Method Calculation Example (TSM)

Suppose we were just given two assumptions for our illustrative exercise:

- Current Share Price = $20.00

- Basic Shares Outstanding = 10mm

If we were to ignore the dilutive impact of non-basic shares in the calculation of equity value, we would arrive at $200mm.

- Equity Value = $20.00 x 10mm = $200mm

However, since we are accounting for the impact of potentially dilutive securities, we must calculate the net impact from in-the-money options. Here, we have three different tranches of options.

- Tranche 1 → 100mm Potential Shares @ $10.00 Strike Price

- Tranche 2 → 200mm Potential Shares @ $15.00 Strike Price

- Tranche 3 → 250mm Potential Shares @ $25.00 Strike Price

The formula for calculating the net dilution from each tranche of options contains an “IF” function that first confirms that the strike price is less than the current share price.

If the statement is true (i.e., the options are exercisable), then the associated number of potential new shares issued is output.

Here, the current share price exceeds the strike price for the first two tranches ($10 and $15) but not the third tranche ($25).

Considering how TSM assumes the company repurchases shares at the current share price, thus the strike price is multiplied by the number of potential new shares, before being divided by the current share price.

4. Treasury Stock Method Analysis (TSM)

The difference between the number of shares assumed to have been issued related to the dilutive securities and the number of shares repurchased as part of TSM is the net dilutive impact.

In the last part of the formula, the number of shares repurchased is deducted from the total potential shares issued to calculate the net dilution, which is completed for each of the three option tranches.

By multiplying the fully diluted shares outstanding by the current share price, we calculate that the net impact of dilutive securities is $2mm and the diluted equity value is $202mm.

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today

")

")