- Walk Me Through a DCF

- How to Answer the "Walk Me Through a DCF" Interview Question

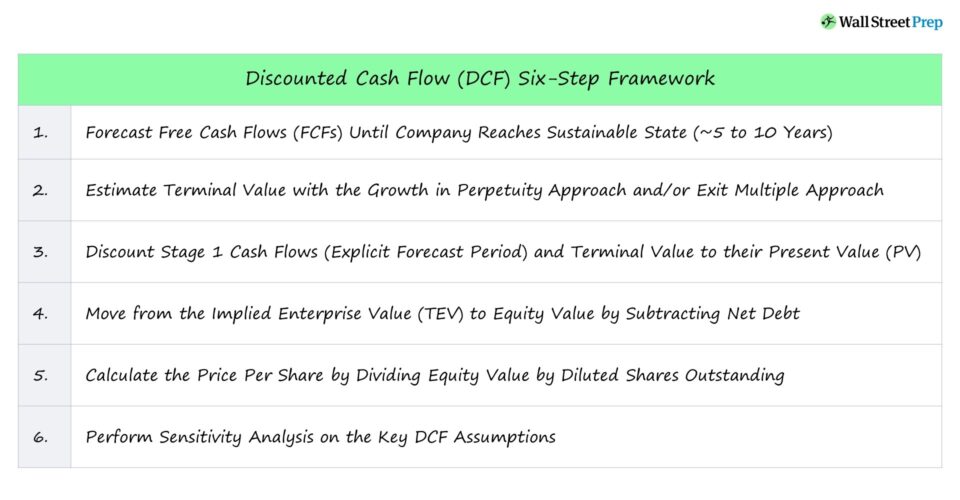

- 2-Stage DCF Model Structure Overview

- Step 1. Initial Forecast Period (Stage 1)

- Step 2. Calculate Terminal Value

- Step 3. Discount Stage 1 Cash Flows and Terminal Value

- Step 4. Calculate Equity Value from Enterprise Value

- Step 5. Calculate Equity Value Per Share

- Step 6. Sensitivity Analysis

- Concluding Tips on Answering "Walk Me Through a DCF"

Walk Me Through a DCF

If you’re recruiting for investment banking or related front-office finance positions, “Walk Me Through a DCF” is almost guaranteed to be asked in an interview setting.

In the following post, we’ll provide a step-by-step framework for answering the common DCF interview question – as well as the common pitfalls to avoid.

How to Answer the “Walk Me Through a DCF” Interview Question

The discounted cash flow analysis (DCF), in short, is one of the core valuation methodologies used in corporate finance.

Questions regarding the DCF should be expected in interviews for practically all front-office finance interviews for investment banking, private equity, and public equities investing.

The premise of the DCF valuation method states that a company’s intrinsic value is equal to the sum of the present value (PV) of its projected free cash flows (FCFs).

The DCF model is considered a fundamental approach to valuation due to estimating a company’s intrinsic value.

Since the DCF values a company as of the present date, the future FCFs must be discounted using a rate that appropriately accounts for the riskiness of the company’s cash flows.

Learn More → Investment Banking Primer

2-Stage DCF Model Structure Overview

The standard DCF model is the two-stage structure, which is comprised of:

- Stage 1 Forecast: The financial performance of the company is projected between five to ten years using explicit operating assumptions.

- Terminal Value: The 2nd stage of the DCF is the value of the company at the end of the initial forecast period, which must be estimated with simplifying assumptions.

Step 1. Initial Forecast Period (Stage 1)

The first step to performing a DCF analysis is to project the company’s free cash flows (FCFs).

The FCFs are projected until the performance of the company reaches a sustainable state where the growth rate has “normalized.”

Typically, the explicit forecast period – i.e. the Stage 1 cash flows – lasts for around 5 to 10 years. Beyond 10 years, the DCF and assumptions gradually lose reliability, and the company might be too early in its lifecycle for the DCF to be used.

The type of free cash flows (FCFs) projected has significant implications for the subsequent steps.

- Free Cash Flow to Firm (FCFF) – FCFF pertains to all providers of capital to the company, such as debt, preferred stock, and common equity.

- Free Cash Flow to Equity (FCFE) – FCFE is the residual cash flows that flow solely to common equity, as all cash outflows related to debt and preferred equity were deducted.

In practice, the more common approach is the unlevered DCF model, which discounts the cash flows to the firm prior to the impact of leverage.

To project the free cash flows (FCFs) of the company, operating assumptions regarding the company’s expected financial performance must be determined, such as:

- Revenue Growth Rate

- Profitability Margin (e.g. Gross Margin, Operating Margin, EBITDA Margin)

- Reinvestment Rate (i.e. Capital Expenditures and Net Working Capital)

- Tax Rate %

Step 2. Calculate Terminal Value

With the Stage 1 forecast done, the value of all the FCFs past the initial forecast period must then be calculated – otherwise known as the “terminal value”.

The two approaches for estimating the terminal value are as follows:

- Growth in Perpetuity Approach – A constant growth rate assumption typically based on the rate of GDP or inflation (i.e. 1% to 3%) is used as a proxy for the company’s future growth prospects into perpetuity.

- Exit Multiple Approach – The average valuation multiple, most frequently EV/EBITDA, of comparable companies in the same industry is used as a proxy for the valuation of the target company in a “mature” state.

Step 3. Discount Stage 1 Cash Flows and Terminal Value

Since the DCF-derived value is based on the present date, both the initial forecast period and terminal value must be discounted to the current period using the appropriate discount rate that matches the free cash flows projected.

- FCFF → Weighted Average Cost of Capital (WACC)

- FCFE → Cost of Equity (CAPM)

The WACC represents the blended discount rate applicable to all stakeholders – i.e. the required rate of return for all capital providers and the discount rate used for unlevered FCFs (FCFF).

In contrast, the cost of equity is estimated using the capital asset pricing model (CAPM), which is the required rate of return by holders of common equity and is used to discount levered FCFs (FCFE).

Step 4. Calculate Equity Value from Enterprise Value

The unlevered and levered DCF approaches begin to diverge around here, as the unlevered DCF calculates the enterprise value whereas the levered DCF calculates the equity value directly.

To move from the enterprise value to the equity value, we must subtract net debt and any other non-equity claims such as non-controlling interest to isolate the common equity claims.

To calculate the net debt, we add the value of all non-operating cash-like assets such as short-term investments and marketable securities, and then subtract from debt and any interest-bearing liabilities.

Step 5. Calculate Equity Value Per Share

The equity value is divided by the total diluted shares outstanding as of the valuation date to arrive at the DCF-derived share price,

Since public companies often issue potentially dilutive securities such as options, warrants, and restricted stock, the treasury stock method (TSM) should be used to calculate the share count – otherwise, the price per share will be higher due to neglecting the extra shares.

If publicly traded, the equity value per share – i.e. the market share price – that our DCF model calculated can be compared to the current share price to determine if the company is trading at a premium or discount to its intrinsic value.

Step 6. Sensitivity Analysis

No DCF model is complete without performing sensitivity analysis, especially considering the DCF’s sensitivity to the assumptions used.

In the final step, the most impactful variables on the implied valuation – typically the cost of capital and terminal value assumptions – are entered into sensitivity tables to assess the impact these adjustments have on the implied value.

Concluding Tips on Answering “Walk Me Through a DCF”

Focusing on the “big picture” when answering the DCF question forces you to think more clearly about the concepts that actually matter.

In short, keep your response concise and get straight to the point.

One common mistake is the tendency to ramble during the interview while going on unnecessary tangents.

The interviewer is just confirming that you have a baseline understanding of the DCF concepts.

Therefore, it’ll be in your best interests to focus on the “high-level” steps, as doing so shows that you can distinguish between the important DCF features and any minutiae.

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today

")

")